Articles & Questions

Every week I publish a fun new article on a money topic I think you’ll find interesting. I also answer a handful of reader questions. Subscribers to my newsletter get to see everything first — but you can browse some of my past articles & questions on this page.

My Best Articles

Not sure where to start? Below I’ve handpicked a few of my favourites. And if you like what you see, don’t forget to subscribe to my free newsletter to get new issues before anyone else!

Search Articles

Australia's Youngest Property Owner

Picture this, it’s April 26. 3:30pm.

Picture this, it’s April 26. 3:30pm.

Malcolm Turnbull and Scott Morrison are deep in the ‘burbs.

The media pack is in tow, getting ready for a photo opportunity.

Today’s pitch? That negative gearing is the way everyday Aussies (voters) get rich -- and, unlike Labor, the Government won’t mess with it.

The Prime Minister peeks through the front door and surveys the battler family.

Turnbull: “He looks ethnic. She’s a blonde. They have a baby. All my ‘demos’ covered under one roof. Excellent.”

Sco-Mo: “Mal, before we go in … there’s just one thing … the apartment. It’s for the kid.”

Turnbull: “What?!”

Sco-Mo: “It’s negatively geared … for the one-year-old.”Turnbull: “Oh for christsakes. Who organised this sh…oot? It was one of Tony’s old staffers, surely?!

Sco-Mo: “It’s too late to back out now. The cameras are rolling. Just smile. It’ll be all over soon.”

A few awkward minutes later, and with the media money shot in the can, it was all over. Yet while there was a lot of fanfare, the only person who didn’t get their say was Australia’s youngest homeowner, baby Addison. So let’s fill her in with what’s going on.

A letter to Baby Addison

Dear Addison,

Your parents love you.When I was a one-year-old all I got was second-hand cigarette smoke, and a Melbourne Footy Club beanie. Your parents bought you a home!

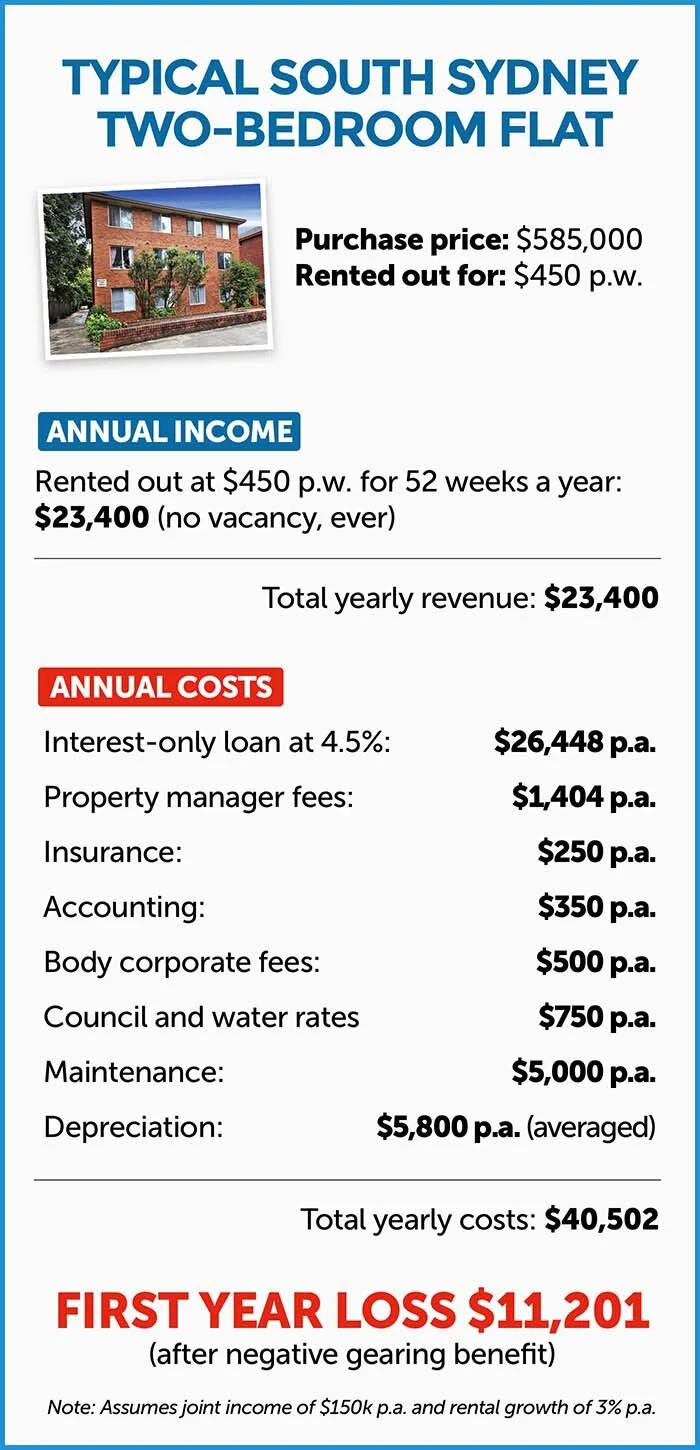

Now, given you’re already crawling up the property ladder, it’s time we had a grownup chat about the true costs of being a property investor in 2016. See, despite interest rates being at all-time lows, your parents will actually lose money on your apartment every single year.

Let’s take a look at the numbers:

First, before your parents got the keys they had to shell out $22,144 in stamp duty, plus legals.

Then, even if we factor in healthy renting increases and an unlikely 100 per cent tenancy -- over the next 20 years they’ll lose $237,900 (see box).

Boo! Hiss!

Yet they’ll also get an annual negative gearing tax break, which will lessen their total after-tax losses to $155,800. Or, looked at another way, the hard-working nurse who delivered you (along with every other taxpayer) will chip in $82,100 over the next 20 years to help fund your loss-making investment.

So on very conservative figures, your parents will lose $178,944 over the next 20 years.

Now the majority of property investors today have absolutely no problem with that.But I do.I hate the idea of losing money every single year for 20 years -- even if I’m getting a tax break. Call me old-fashioned, but when I invest my hard earned money I expect my investments to put money in my pocket every single year.

And when I reinvest my returns each year, I’m getting something known as compound interest. Albert Einstein called it the eighth wonder of the world. That’s because, over time, you earn interest on your interest, and your returns snowball.

That’s the guaranteed way to get very, very rich.

But that’s not going to happen for you, unfortunately.

Your apartment won’t get the benefits of compound interest, because every last dollar of income (in the form of rent) that your parents receive, is completely gobbled up by your costs: to the bank, and to keeping the apartment. The only way your parents will make money is if the price of the apartment increases.

The Alternative: Create A Bond With Your Kid

But let’s be old-fashioned.

Instead of losing money each year, let’s save.

Now let’s run the numbers on investing the same amount that your parents will lose over the next 20 years in a low-cost, old-school investment bond, invested in an Aussie managed share fund.

For argument’s sake we’ll say your parents kick it off with $23,144 (what they paid in stamp duty and legal fees) plus what they lose (after tax) every year into the investment bond (which, as I’ve said, totals $155,800 after 20 years).

Assuming a conservative after-tax 6 per cent return, and annual investment fees of 0.78 percent, in 20 years your bond will be worth … $364,563.

A good deal for you, but an even better deal for your parents.

Here’s how I’d sell it to them, Addison.

“Mum and Dad, if you fund my future with savings, instead of debt, you’ll feel a lot less pressure. You won’t have to worry about losing your job, or not being able to fund the shortfall.”

(Which in the first year is approximately 10 per cent of your take-home pay.)

“You won’t have to worry about interest rates jacking up.”

(Let’s face it, interest rates won’t stay at a historical low for the next 20 years.)

“You won’t have to worry about your tenants breaking things, or leaving you in the lurch.”

(The figures we’ve used factor in a 100 percent tenancy over 20 years -- which won’t happen.)

“You won’t have to worry about greedy land tax grabs from the State Government.”

(They’ve got form here.)

“You won’t have to worry about changes to negative gearing.”

(Which, like changes to super, could change the game completely).

“You won’t have to worry about paying another round of stamp duty when you transfer the apartment to me in 20 years’ time.”

(Which will eat up another 4 per cent of your capital.)

“You won’t have to worry about paying capital gains tax at the end of it.”

(Investment bonds are totally free from capital gains tax free after 10 years.)

“So, Mum and Dad, for all these reasons I think you’ll agree it makes sense to save, rather than speculate. And besides, if you do, you won’t have set a precedent to buy my future brothers or sisters their own negatively geared apartment, which on these figures you won’t be able to afford … even with negative gearing!”

Tread Your Own Path!

Real Estate Mistakes: How to Turn $90,000 into $2.4 million

I’m writing this to you today from my study, which overlooks the rolling hills of my family farm. It’s really peaceful out here.

I’m writing this to you today from my study, which overlooks the rolling hills of my family farm. It’s really peaceful out here.

And, if you drive up to the top of those rolling hills, you can catch a glimpse of a smaller farm that’s just down the road, which was once marketed as Secret Valley.

“Set 45 minutes from the Melbourne CBD, the Secret Valley Estate is 258 acres of breathtaking, beautiful landscape and picturesque views of the Macedon Ranges.”

A few years ago, busloads of property investors would do field trips to Secret Valley.

They’d wander around the paddocks, sizing up what they were told was a canny investment.

The idea was simple: Secret Valley is on the edge of the Melbourne sprawl. Eventually it will be swallowed up by suburbia. And if you were smart enough to own an option on a few plots of land in the Secret Valley Estate, well, you could become very, very rich.

How rich?The marketing pitch that got the property investors on the bus was that if you invested $120,000 you could turn it into $1.2 million.

OK, so if you’ve been reading my column for a while, you won’t be surprised to hear that the investors in Secret Valley got roughly the same treatment that my ewes receive when I put a few daddy rams into the paddock.

A few years on, the only secret around Secret Valley is where all the investors’ loot ended up.

That case is still before the courts, which means I can’t really comment.

So to learn a bit more about “land banking”, as it’s known, I called up an old spiv who was up to his neck in it years ago.

He told me that he’d explain how the game worked, on one condition: that he be totally anonymous. Which is totally understandable … especially when you read what he says.

HERE’S his explanation of how land banking works in the get-rich-quick market:

“You buy rural land for $10,000 an acre. You then turn around and market it to investors as a ‘rezoning opportunity’. The sales pitch is that investors could make 10 times their money when it’s developed. The investors think they’re on a winner, and they’ll fight to buy that same acre for $400,000 a pop. All up, you’ve turned a $90,000 investment into $2.4 million.”

So how is it possible to convince people to buy these plots of land?

He explains:

“You need the best salespeople, and the best salespeople are women. There aren’t many of course, but they’re absolutely dynamite. No one thinks a woman will rip you off, right?

“It works like this. They make three calls.

“The first is to deliver a brochure — something elaborate, expensive, and high quality — lots of bullshit.

“The second call is to find out how much money they have. No one wants to waste their time. They’re getting to know the investor, asking about their kids and stuff, but really all they’re doing is drilling down to see if they have any money.

“This is where it’s easy. Most people have access to their retirement funds. That’s the big opportunity … that’s the honeypot! They look upon it as dead money and are willing to gamble with it. They’re a bit more wet behind the ears in Australia — they have this belief that property never goes down.

“The third call is to land the sale. If you have a client who has money, they’ll pull the trigger. However, you don’t just want to sell a piece of field for $10,000 to a guy who has $1 million. You want to flog him more. The technical term is ‘load up the client’. Generally, if they buy once, they’ll buy five times.”

“LOOK,” he continues, “I graduated from doing small time deals. Suddenly I went from having no money in my account to having $750,000 … in three weeks.

“It’s a fool’s paradise, though, because it doesn’t last. It never lasts. You’re earning $200,000 a month, so you buy a fancy car and you fly first class. But then everything catches up with you. The press catches on to it, investors get shirty, and instead of earning $200,000 a month, you’re earning $20,000.

“I didn’t feel good about myself when I was doing it. Of course. I had really low self-esteem. I drank a lot to block out the reality. I didn’t feel worthy, so I got rid of the money as quickly as I could.

“The truth is that I even got scammed myself by another crowd. Overall, I think I turned over $15 million. You’d expect me to have $10 million. I don’t.”

SO how did it end?“

We could have sold more plots if it weren’t for articles in the newspapers. That’s what screwed us up. People would Google stuff and it made our job almost impossible. We ended up closing ourselves down and heading overseas — the writing was on the wall.”

Except it wasn’t.

This old spiv left the game seven years ago. In the meantime, there’s been land banking schemes from Bendigo to Ballarat, from Shepparton to Secret Valley. It’s been reported that, in the past few years, thousands of Aussie investors have sunk more than $100 million — and possibly as much as $300 million — into land banking schemes. Strewth!

So, as I wrap this column up, there’s probably one last question left unanswered:

Aren’t I effectively doing a bit of “land banking” with my farm?

No.

As I type this I’m watching a few grain-fed sheep fertilise my drought-ravaged paddocks. Seriously, there are better investment opportunities going round. But ... it sure is peaceful out here.

Well, most of the time.

Tread Your Own Path!

Are we in a housing bubble?

Are prices going to crash by as much as 50 per cent, as some experts predicted in the news this week? Will the government have the ticker to change the negative gearing rules?

Are prices going to crash by as much as 50 per cent, as some experts predicted in the news this week?

Will the government have the ticker to change the negative gearing rules?Well, to answer these questions, and offer some views on livestock, this week I caught up with none other than the newly crowned Deputy Prime Minister of Australia, Barnaby Joyce.

And in doing so, I worked out we actually have quite a lot in common: we’re both country blokes. We both have a love of numbers. And we both have a habit of saying whatever’s on our minds at the time.

Barefoot: “Thank-you for your time Deputy Prime Minister. I currently own two Alpacas on my farm, and I just don’t care for them at all. They’re more stubborn than Greens Senator Sarah Hanson Young. Have you ever been spat on by an alpaca...or a Greens supporter?”

Barnaby: “No, although I’ve actually had alpacas run alongside me as I go for a jog down the side of my road. They just look like too much…hard work”.

Barefoot: “First home buyers have the footprints of property investors squarely on their backs. Negative gearing has created an uneven playing field because they can write off their losses against their tax. Explain to me how this is fair or productive?”

Barnaby: “Well….there are affordable houses, there just mightn’t be affordable houses in the places you’re looking. When people say there’s no affordable houses, well that’s not correct, there are, and in regional areas they’re vastly more affordable than in the cities”.

“Look I bought a house in St. George in South-West Queensland. I lived out at Charleville, now I’m living south-of Tamworth, but here’s the thing: I’m still out of town where it’s cheaper. What I’m saying is you’ve got to look across the nation. If you look around and say the houses around me are unaffordable you’ve got to ask yourself... is there somewhere else you can go where they are affordable?”.

Barefoot: “So what you’re basically saying is the Government doesn’t have the ticker to touch negative gearing, right?”

Barnaby: “The problem you’re going to have is that if you start messing around in any place without a proper plan, the problems you can create can be vastly greater than the problems you had. If you go into any market and take a substantial group of people out of that market, you can have an incredibly detrimental effect on all the people who have currently bought a house. There’s two sides to every equation”.

Barefoot: “Yes, but there is a substantial group of people who right now are priced out of the housing market. They’re called first home buyers”.

Barnaby: “There are two groups of people who you always have to consider: the people who want to get in and the people who are already there. So it’s never a simple equation, if you’re going to say I’m going to make all houses cheaper, you’ve just made all the people who own houses or owe money to a bank on a house, poorer”.

So here’s my take out from my discussion with the Deputy Prime Minister.

There is absolutely zero chance the government will do anything more than fiddle around the edges of negative gearing policy.

As Barnaby says there are two sides to every equation -- and make no mistake, in politics the side that wins is usually the one with the most voters -- and roughly two-thirds of Australian voters are homeowners.

It makes perfect political sense: who the hell wants to be remembered as the government that pricked the biggest housing bubble in history?

Well, I’ll tell you who: Bill Shorten.

He’s got nothing to lose, so he’s prepared to roll the dice, and end negative gearing for existing homes.It’s bold, and it’s brassy.

But there’s just one little problem with it: getting Aussies off negative gearing, is alike a junkie getting off the gear. Long-term it’s totally the right thing to do. Just not today...maybe tomorrow (but probably not). The scary part is that everyone knows there will be a withdrawal period, and it will be nasty, and no one can accurately predict what will happen. But let's have a go...

Bill Shorten has said that if he’s elected, negative gearing on existing properties will be axed on the 30th June 2017. However, he’s also assured landlords (and his party) that anyone who buys before that, gets grandfathered tax deductions for life.

So, what do you reckon the property market will do in the run up to the cut off date?

Boom, baby!

What will happen the day after?

Will we be shivering in in a corner, with our heads in a bucket?

Who knows?

Either way we should encourage our politicians to make hard, courageous decisions, that benefit the country in the long-term. However the trouble is for a politician, long-term isn’t even a three year electoral cycle these days -- just ask Kevin, (and Julia and Tony).

So where does that leave first home buyers, with the likelihood that the Barnaby and his boys will be returned to power?

Well, last year the former Treasurer, Smoke’n Joe Hockey’s advice to young people who were struggling to crack into the Sydney property market was to ‘get a good job that pays good money’ (teachers, nurses, police-women, scientists... no house for you. Lawyers, bankers, politicians, you win!).

When I asked Barnaby the same question, here’s what he said:“

The great thing about Australia is if you’ve still got the drive, if you’ve still got the mongrel about you that wants to get up and go, you’ll get there. But if you think you’re going to – by some stroke of luck – walk into a multi-million dollar place for a couple hundred thousand bucks, well that just ain’t going to happen. Like everything in life you’ve got to start from the bottom, work hard and you’ll get there”.

Tread Your Own Path!

Real Estate Mistakes

Have you ever dreamt of building a multimillion-dollar investment portfolio? Travelling overseas — business class — while you live off your six-figure-a-year passive income?

Have you ever dreamt of building a multimillion-dollar investment portfolio?

Travelling overseas — business class — while you live off your six-figure-a-year passive income? If you have, today I’ve got a real treat for you.

This week I caught up with two of the most successful property investors of the past few years.

Kate and Matt Moloney are a twenty-something couple originally from country Victoria. Yet they are anything but typical: they built an $8.5 million property empire, generating $570,000 a year in rental income, in just three years.

In 2012, Kate and Matt were recognised for their achievements, being crowned “Investors of the Year” by Your Investment Property magazine. A panel of five industry experts pored over their portfolio and, after much deliberation, awarded them the prestigious prize.

The entrants were described as “some of the country’s most shrewd investors” and “property powerhouses who are showing the rest of Australia how it’s done”.

“These are ordinary, everyday Australians who have chosen to make a difference in their lives through property investing. By showing fortitude, the willingness to take risks and a sense of the gigantic opportunity that is Australian property, they’ve strived ahead and offer a shining example of how to succeed,” said the magazine.

And specifically: “The young couple wowed our judges with their awe-inspiring ability to get together property finance, even in times when they’ve been without savings or equity.”

Hang on. Hold your horses.

Let’s back up the nag and take a look-see at that last quote: the judges were “wowed” with their “awe-inspiring ability” to borrow money “without savings or equity”?

Uh-huh. We’ll mark that down. Let’s keep going.“The truly remarkable part is that both are just aged 24 and now in a position to semi-retire”, gushed the magazine, which put the couple on the front cover.

“We’re heading on our first round-the-world trip — business class. We’re quitting our jobs and heading to Africa, North America and Europe for a well-earned rest,” said Matt.

“We’ve done the hard yards, starting our investing when we were teenagers, and now we just want to enjoy ourselves,” said Kate.

You can picture them, can’t you?

They’ve got their “Investors of the Year” Oscar-like trophy wedged into their Gucci carry-on luggage. They’re reclining in their plush leather seats, triumphantly clinking their champagne glasses as the pointy end of the plane lifts off the tarmac bound for the bright lights of New York City.

Meanwhile the rest of us are stuck in peak-hour traffic — spilling coffee on our shirts — and cursing the cost of affording a dog box in Bendigo, much less owning a multimillion-dollar property portfolio.

And Kate and Matt lived happily ever after, right? Well, no.This story doesn’t end in the business class lounge, but three years later in the bankruptcy court.Yes, today Kate and Matt are bankrupt.

Well, not officially — though I assured them this week that it’s definitely going to happen, and soon.

That’s because they currently owe $5.8 million on their investment property portfolio. The value of these properties (mostly bought in the mining boom-and-bust town of Moranbah, Queensland) has plummeted to a paltry $2.3 million today. In other words, they’re $3.5 million underwater on their loans.

To make matters worse, both Matt and Kate are currently not working. But it wasn’t losing their jobs that did them in — the seeds of their financial cancer were sewn back in 2009 when they paid $7000 to attend a property seminar from an outfit called Real Wealth Australia and they got well and truly swept up in the rah-rah.

It was at the course that Kate and Matt ditched their half-paid-off marital home in country Victoria and set their eyes on becoming miyonaires! The strategy was simple: buy multiple investment properties in mining towns.

I mean, what could be better than buying one investment property?

Buying 20.A few years later — having well and truly sucked the spruiker juice — Kate and Matt attended a $4000 workshop hosted by Dymphna Boholt, who says on her website that “educating on success, money, and material wealth are the things that I am best known for”. (To be fair, she’s also known for making misleading claims that have been exposed by the ACCC and Fair Trading Queensland.)

They were so motivated by Boholt’s first seminar that they ended up graduating to her platinum mentoring service, which cost $30,000. For that money, says Kate, Dymphna was recommending investing in mining towns.

Kate also alleges that some people she was dealing with throughout her buying binge were receiving kickbacks on the debts she was taking out, though she says it was never disclosed to her.

The problem is that this young couple from the country were unwittingly held up as poster kids of success, and their story was used to suck more people into the get-rich-quick schemes.

“The spruikers would fight over us. They’d get us up on stage with the motivational music blaring. Each claimed that it was their course that had turned us into multi-millionaires in a few years,” said Kate.

“But it was all built on lies. Even our capital city properties were sold for huge losses.”

The hard truth that Kate and Matt have learned is that there’s no shortcut to any place worth going.

They’ve also learned that Your Property Investor magazine is the equivalent of a porno for property punters. (Though I’d argue they’re not so much Playboy — more like Hustler.) Seriously, it’s so sleazy that they should sell it wrapped in cellophane.

By the way, I didn’t get away scot free on this one either. In researching this column on the interwebs, I found there are a lot of investment property gurus who really don’t like me: “The Barefoot Investor gives commonsense, simple and incredibly boring savings advice”, said one.

Bit harsh!

Then again, if Kate and Matt had followed the Barefoot path, they’d own their own (modest) home today — before they turned 30.

And here’s the thing: once you knock out your biggest payment, your financial world changes: You can build a multimillion-dollar investment portfolio, you can semi-retire, and you can even save up and enjoy an around-the-world trip … business class.

Tread Your Own Path!

P.S Kate told her story last night on 60 Minutes.

All week Channel Nine had been promoting it as ‘the next great mortgage disaster’.

Last night I got to see the story, and it was … rubbish.

I was looking for an intelligent discussion on the dangers of an investor-led boom. Or perhaps a pointer of the role that property spruikers played in pumping up prices in investor-ghettos (mining towns, student accommodation, inner city dog boxes, government supported NRAS housing, negative gearing).

Nope.

Our flagship investigative show suggested that house prices in the mining town of Moranbah -- which saw its median house price jump by as much as $500,000...then plummet by as much as $600,000 -- is comparable to what is going to happen in suburban Australia.

That assumption, to quote my toddler Louie is “Ri-dic-orus”.

Finally, if you want a fly on the windscreen account of the sleazy world of the property seminar circus, buy Kate’s book. Goodness knows she needs the money.